Another type of auto fraud related to the vehicle's financing is when the dealer incorrectly discloses the financial terms of the loan. This dishonest practice is designed to dupe the buyer into thinking that the loan is more favorable than it really is.

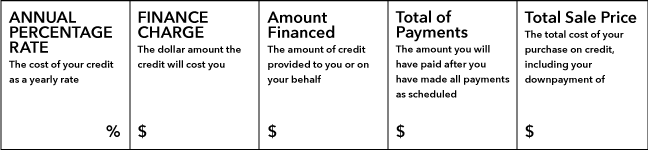

Under the Truth in Lending Act, the dealer must accurately disclose the amount financed, the finance charge, and the annual percentage rate. Federal law requires that these terms be disclosed in the so-called Truth in Lending box (pictured above). The main point of the Act is to require transparent and consistent disclosure of finance terms so that buyers can easily compare multiple loans and decide which one is best.

Here's what the key terms mean:

Amount Financed. This is the total amount of money you are borrowing from the lender.

Finance Charge. These are all of the charges imposed as a result of the extension of credit. This obviously includes interest, but should also include any other charge that a buyer would not have to pay if it was a cash transaction.

What a shady dealer might do is to manipulate these disclosures to distort the true cost of the credit. The most common way a dealer does this is add a finance-related charge to the "Amount Financed" total rather than the "Finance Charge" total. This little trick will make the interest rate look lower than it really is.

Here's an example. Let's say you're buying a used car for $10,000. The annual interest rate is 10% and you will pay it off over 5 years (60 months). So the $10,000 would go in the Amount Financed box because it's the amount you're borrowing. And the interest amount ($2,621.25) would go in the Finance Charge box.

Because you're financing the transaction, the dealer requires that a GPS unit be installed so that it can locate the vehicle for a repossession if you fall behind on payments. The dealer charges you $500 for the GPS unit. Because the dealer allows you to roll this $500 charge into your loan, it goes in Amount Financed box right? Wrong. The GPS fee should be a Finance Charge because the dealer only requires these GPS units for buyers that finance. It doesn't require them for cash buyers. By fraudulently putting the GPS fee into the Amount Financed box, the dealer keeps the APR at 10%. But if the GPS fee was put in the Finance Charge box where it belongs, the APR jumps to 12.33%. You can verify my math if you like by using this online APR calculator.

The takeaway? Make sure you carefully review the terms of your loan to make sure the dealer isn't trying to scam you. Review every charge and ask yourself would the dealer charge this in a cash transaction? If the answer is no, then it should be a finance charge and disclosed accordingly. If the dealer improperly discloses the financial terms or misstates the interest rate, it likely has violated the Truth in Lending Act. This would give rise to claims for statutory damages, actual damages, and the dealer would have to pay your attorney fees and court costs.